Shift of global economic power to emerging economies set to continue in long run, with India, Indonesia and Vietnam among star performers

02/07/17

Latest PwC report projects that for GDP measured at purchasing power parities (PPPs):

- World economy could double in size by 2042

- China has already overtaken the US to be largest economy based on GDP in PPP terms, and could be the largest valued at market exchange rates before 2030

- India could overtake the US by 2050 to go into 2nd place and Indonesia could move into 4th place by 2050, overtaking advanced economies like Japan and Germany

- By 2050, six of the seven largest economies in the world could be emerging markets

- Vietnam could be the world’s fastest growing large economy over the period to 2050, rising to 20th in the global GDP rankings by that date

- Turkey could overtake Italy by 2030 if it can overcome current political instability and make progress on economic reforms

- Nigeria has potential to rise up the global GDP rankings, but only if it can diversify its economy and improve governance standards and infrastructure

7th February, 2017 – The long-term global economic power shift away from the established advanced economies is set to continue over the period to 2050, as emerging market countries continue to boost their share of world GDP in the long run despite recent mixed performance in some of these economies.

This is one of the key findings from the latest report from PwC economists on the theme of the World in 2050: The long view: how will the global economic order change by 2050? This presents projections of potential GDP growth up to 2050 for 32 of the largest economies in the world, which together account for around 85% of global GDP. These projections are based on the latest update of a detailed long-term global growth model first developed by PwC in 2006.

The report projects that the world economy could double in size by 2042, growing at an annual average real rate of around 2.5% between 2016 and 2050. This growth will be driven largely by emerging market and developing countries, with the E7 economies of Brazil, China, India, Indonesia, Mexico, Russia and Turkey growing at an annual average rate of around 3.5% over the next 34 years, compared to only around 1.6% for the advanced G7 nations of Canada, France, Germany, Italy, Japan, the UK and the US.

John Hawksworth, PwC Chief Economist and co-author of the report, comments:

“We will continue to see the shift in global economic power away from established advanced economies towards emerging economies in Asia and elsewhere. The E7 could comprise almost 50% of world GDP by 2050, while the G7’s share declines to only just over 20%”

Table 1 below sets out how PwC projects global GDP rankings at PPPs (see Note 1) will evolve.

Table 1: Projected global GDP rankings in PPP terms (US$bn at constant 2016 values)

| 2016 rankings | 2030 rankings | 2050 rankings | ||||

|---|---|---|---|---|---|---|

| GDP PPP rankings | Country | GDP at PPP | Country | Projected GDP at PPP | Country | Projected GDP at PPP |

1 |

China |

21269 |

China |

38008 |

China |

58499 |

2 |

United States |

18562 |

United States |

23475 |

India |

44128 |

3 |

India |

8721 |

India |

19511 |

United States |

34102 |

4 |

Japan |

4932 |

Japan |

5606 |

Indonesia |

10502 |

5 |

Germany |

3979 |

Indonesia |

5424 |

Brazil |

7540 |

6 |

Russia |

3745 |

Russia |

4736 |

Russia |

7131 |

7 |

Brazil |

3135 |

Germany |

4707 |

Mexico |

6863 |

8 |

Indonesia |

3028 |

Brazil |

4439 |

Japan |

6779 |

9 |

United Kingdom |

2788 |

Mexico |

3661 |

Germany |

6138 |

10 |

France |

2737 |

United Kingdom |

3638 |

United Kingdom |

5369 |

11 |

Mexico |

2307 |

France |

3377 |

Turkey |

5184 |

12 |

Italy |

2221 |

Turkey |

2996 |

France |

4705 |

13 |

South Korea |

1929 |

Saudi Arabia |

2755 |

Saudi Arabia |

4694 |

14 |

Turkey |

1906 |

South Korea |

2651 |

Nigeria |

4348 |

15 |

Saudi Arabia |

1731 |

Italy |

2541 |

Egypt |

4333 |

16 |

Spain |

1690 |

Iran |

2354 |

Pakistan |

4236 |

17 |

Canada |

1674 |

Spain |

2159 |

Iran |

3900 |

18 |

Iran |

1459 |

Canada |

2141 |

South Korea |

3539 |

19 |

Australia |

1189 |

Egypt |

2049 |

Philippines |

3334 |

20 |

Thailand |

1161 |

Pakistan |

1868 |

Vietnam |

3176 |

21 |

Egypt |

1105 |

Nigeria |

1794 |

Italy |

3115 |

22 |

Nigeria |

1089 |

Thailand |

1732 |

Canada |

3100 |

23 |

Poland |

1052 |

Australia |

1663 |

Bangladesh |

3064 |

24 |

Pakistan |

988 |

Philippines |

1615 |

Malaysia |

2815 |

25 |

Argentina |

879 |

Malaysia |

1506 |

Thailand |

2782 |

26 |

Netherlands |

866 |

Poland |

1505 |

Spain |

2732 |

27 |

Malaysia |

864 |

Argentina |

1342 |

South Africa |

2570 |

28 |

Philippines |

802 |

Bangladesh |

1324 |

Australia |

2564 |

29 |

South Africa |

736 |

Vietnam |

1303 |

Argentina |

2365 |

30 |

Colombia |

690 |

South Africa |

1148 |

Poland |

2103 |

31 |

Bangladesh |

628 |

Colombia |

1111 |

Colombia |

2074 |

32 |

Vietnam |

595 |

Netherlands |

1080 |

Netherlands |

1496 |

Sources: IMF for 2016 estimates (with an update for Turkey), PwC projections for 2030 and 2050

When looking at GDP measured at market exchange rates (MER), there is not quite such a radical shift in global economic power. But China still emerges as the largest economy in the world before 2030 and India is still clearly the third largest in the world by 2050.

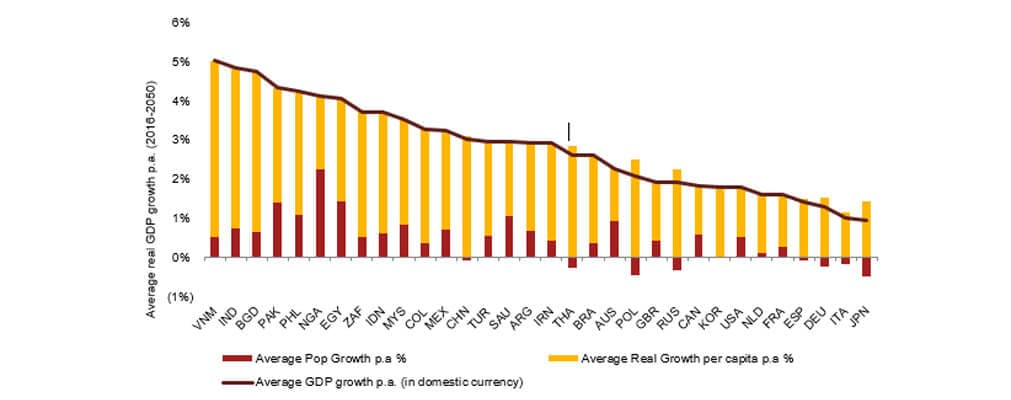

But the spotlight will certainly be on the newer emerging markets as they take centre stage. By 2050, Indonesia and Mexico are projected to be larger than Japan, Germany, the UK or France, while Turkey could overtake Italy. In terms of growth, Vietnam, India and Bangladesh could be the fastest growing economies over the period to 2050, averaging growth of around 5% per year as illustrated in Figure 1, which also shows how growth breaks down between population and GDP per capita.

Figure 1: Projected average real GDP growth per annum, 2016-50

Source: PwC analysis based on UN population projections

Nigeria has the potential to move eight places up the GDP rankings to 14th by 2050, but it will only realise this potential if it can diversify its economy away from oil and strengthen its institutions and infrastructure.

Colombia and Poland also exhibit great potential, and are projected to be the fastest growing large economies in their respective regions, Latin America and the EU (though Turkey is projected to grow faster if we consider a wider definition of Europe).

Says John Hawksworth:

“Growth in many emerging economies will be supported by relatively fast-growing populations, boosting domestic demand and the size of the workforce. This will need, however, to be complemented with investments in education and improvement in macroeconomic fundamentals to ensure there are sufficient jobs for the growing number of young people in these countries.”

Average incomes

One bit of good news for today’s advanced economies is that they will continue to have higher average incomes – with the possible exception of Italy, all of the G7 continue to sit above the E7 in the rankings of GDP per capita in 2050. Emerging markets are projected close the income gap gradually over time, but full convergence of income levels across the world is likely to take until well beyond 2050.

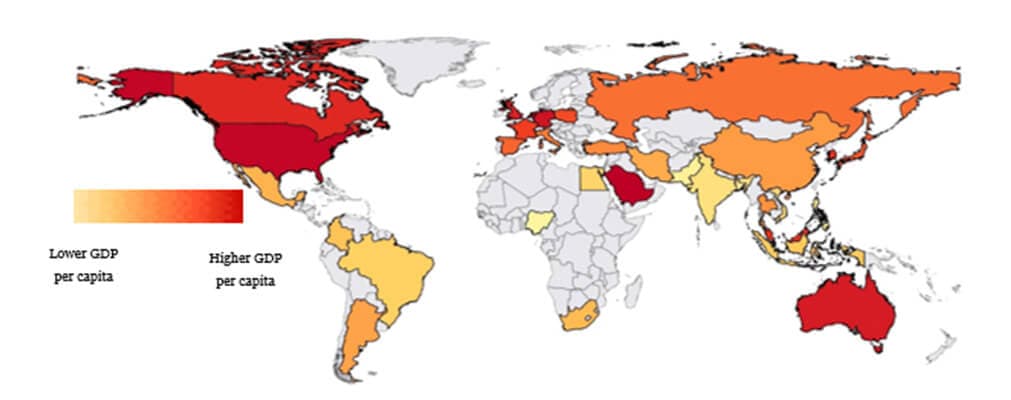

China achieves a middling average income level by 2050 (see Map 1), while India remains in the lower half of the income range given its starting point, despite relative high projected growth over time. This illustrates that while strong population growth can be a key driver of total GDP growth , it will take much longer to eliminate differences in average income levels.

Map 1: Projected real GDP per capita in 2050

Source: PwC projections starting from IMF estimates for 2016

Says John Hawksworth:

“Average income gaps between countries will reduce over time, but this process will still be far from complete by 2050. In 2016, US GDP per capita was almost four times that of China’s and almost nine times that of India’s. By 2050, these gaps are projected to narrow so that average US income levels may be around double China’s and around three times India’s – but it is also possible that income inequality within countries will continue to rise, driven in particular by technological change that favours higher skilled workers and the owners of capital.”

Global growth projected to slow as populations age and emerging economies mature

PwC economists project global economic growth to average around 3.5% per annum over the years to 2020, slowing down to around 2.7% in the 2020s, 2.5% in the 2030s, and 2.4% in the 2040s. This will occur as many advanced economies (and eventually also some emerging markets like China) experience a marked decline in their working-age populations. At the same time, emerging market growth rates will moderate as these economies mature and the scope for rapid catch-up growth declines. These effects are projected to outweigh the impact of emerging economies having a progressively higher weight in world GDP, which would otherwise tend to boost average global growth.

Challenges for policymakers to achieve long-term sustainable growth

To realise their great potential, emerging economies must undertake sustained and effective investment in education, infrastructure and technology. The fall in oil prices from mid-2014 to early 2016 highlighted the importance of more diversified emerging economies for long-term sustainable growth. Underlying all of this is the need to develop the political, economic, legal and social institutions within emerging economies to generate incentives for innovation and entrepreneurship, creating secure and stable economies in which to do business.

Says John Hawksworth:

“Policymakers across the world face a number of challenges if they are to achieve sustainable long-term economic growth of the kind we project in this report. Structural developments, such as ageing populations and climate change, require forward-thinking policy which equips the workforce to continue to make societal contributions later on in life and promotes low carbon technologies.

“Falling global trade growth, rising income inequality within many countries and increasing global geopolitical uncertainties are intensifying the need to create diversified economies which create opportunities for everyone in a broad variety of industries.”

Great opportunities for business with the right strategic mix of flexibility and patience

Emerging market development will create many opportunities for business. These will arise as these economies progress into new industries, engage with world markets and as their relatively youthful populations get richer. They will become more attractive places to do business and live, attracting investment and talent.

Emerging economies are rapidly evolving and often relatively volatile, however, so companies will need operating strategies that have the right mix of flexibility and patience to succeed in these markets. Case studies in the PwC report illustrate how businesses should be prepared to adjust their brand and market positions to suit differing and often more nuanced local preferences. An in-depth understanding of the local market and consumers will be crucial, which will often involve working with local partners.

Concludes John Hawksworth:

“Businesses need to be patient enough to ride out the short-term economic and political storms that will inevitably occur from time to time in these emerging markets as they move towards maturity. But the numbers in our report make clear that failure to engage with these emerging markets means missing out on the bulk of the economic growth we expect to see in the world economy between now and 2050.”

ENDS

Notes:

- PPPs vs MERs: there is no single correct way to measure the relative size of economies at different stages of development. Depending on the purpose of the exercise, GDP at either market exchange rates (MERs) or purchasing power parity rates (PPPs) may be the most appropriate measure. In general, GDP at PPPs is a better indicator of average living standards or volumes of outputs or inputs because this corrects for relative price differences, while GDP at MERs is a better measure of the relative total size of markets for businesses at a given point in time. However, historical evidence shows that MERs will generally, in the long run, tend to move up towards PPPs for emerging economies as their average income levels gradually narrow the gap with the current advanced economies. An econometric equation within the PwC long-term growth model that reflects this historical relationship forms the basis for the projections of GDP at MERs in the report. This also makes the common simplifying assumption that PPP exchange rates remain constant in real terms over time. Projections of MERs are subject to particularly high margins of uncertainty, however, which is why both the report and this media release focus primarily on projections of GDP at PPPs. But Appendix B in the full report also shows projections for GDP at MERs to 2050 for the 32 economies in the study.

- A copy of the full report The long view: how will the global economic order change by 2050? will be published on 7th February 2017 at http://www.pwc.com/world2050

- This report is part of PwC’s wider research programme on the megatrends shaping global economic and business development. More details can be found here: http://www.pwc.co.uk/issues/megatrends/index.jhtml

- More details on business strategies for emerging markets can be found in reports by the PwC Growth Markets Centre, which are available from: https://www.pwc.com/gx/en/services/consulting/international-growth-practice.html

About PwC

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 157 countries with more than 223,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

© 2017 PwC. All rights reserved

Contact us