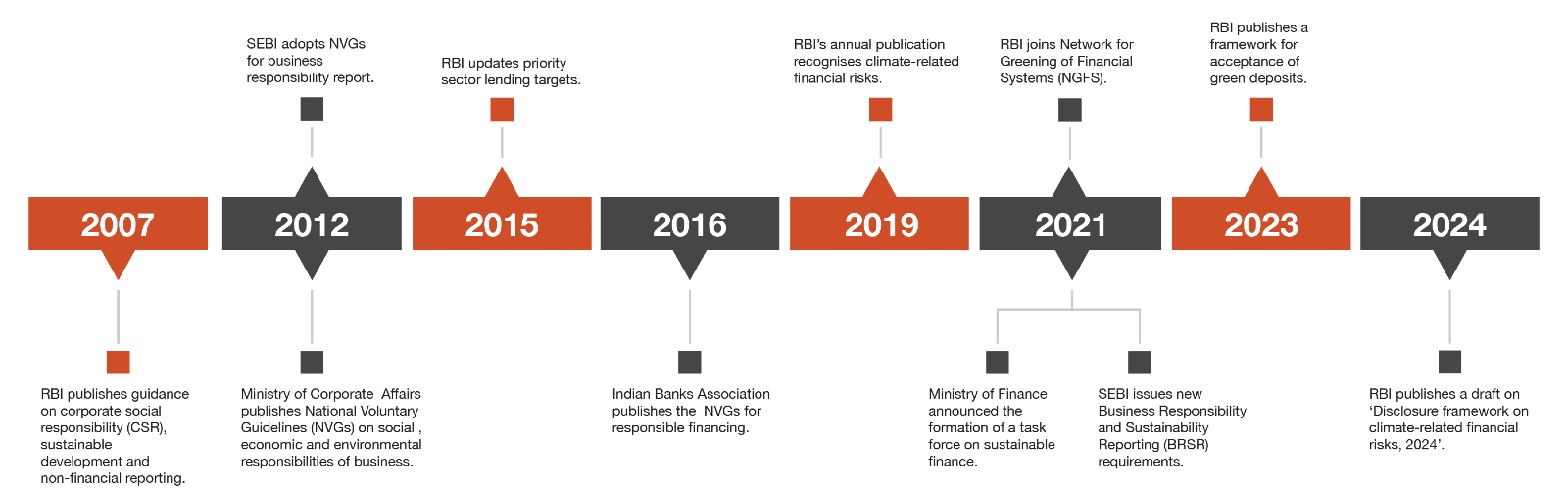

On 28 February 2024, the Reserve Bank of India (RBI) issued draft guidelines on ‘Disclosure framework on climate-related financial risks, 2024’.1 The framework mandates disclosure by regulated entities (REs) on four key areas of governance, strategy, risk management and metric and targets. The central banking regulator recently released a discussion paper on climate risk and sustainable finance2 and the framework for acceptance of green deposits.3 The current disclosure framework is a step towards bringing the climate risk assessment, measurement and reporting requirements under mainstream compliance framework for financial sector entities in India. This move will help incorporate climate-related issues in the overall organisational culture, policies and operations. Given below is a snapshot of the key policy milestones in India’s sustainable and climate finance journey that is being led by the RBI and Government of India.

Key policy milestones in India's sustainable and climate finance journey

Applicability

These guidelines are applicable to all scheduled commercial banks (SCBs) (excluding local area banks, payments banks and regional rural banks), tier-IV primary (urban) co-operative banks (UCBs), All-India Financial Institutions (AIFIs) and top and upper layer non-banking financial companies (NBFCs). Other entities may voluntarily make these disclosures.

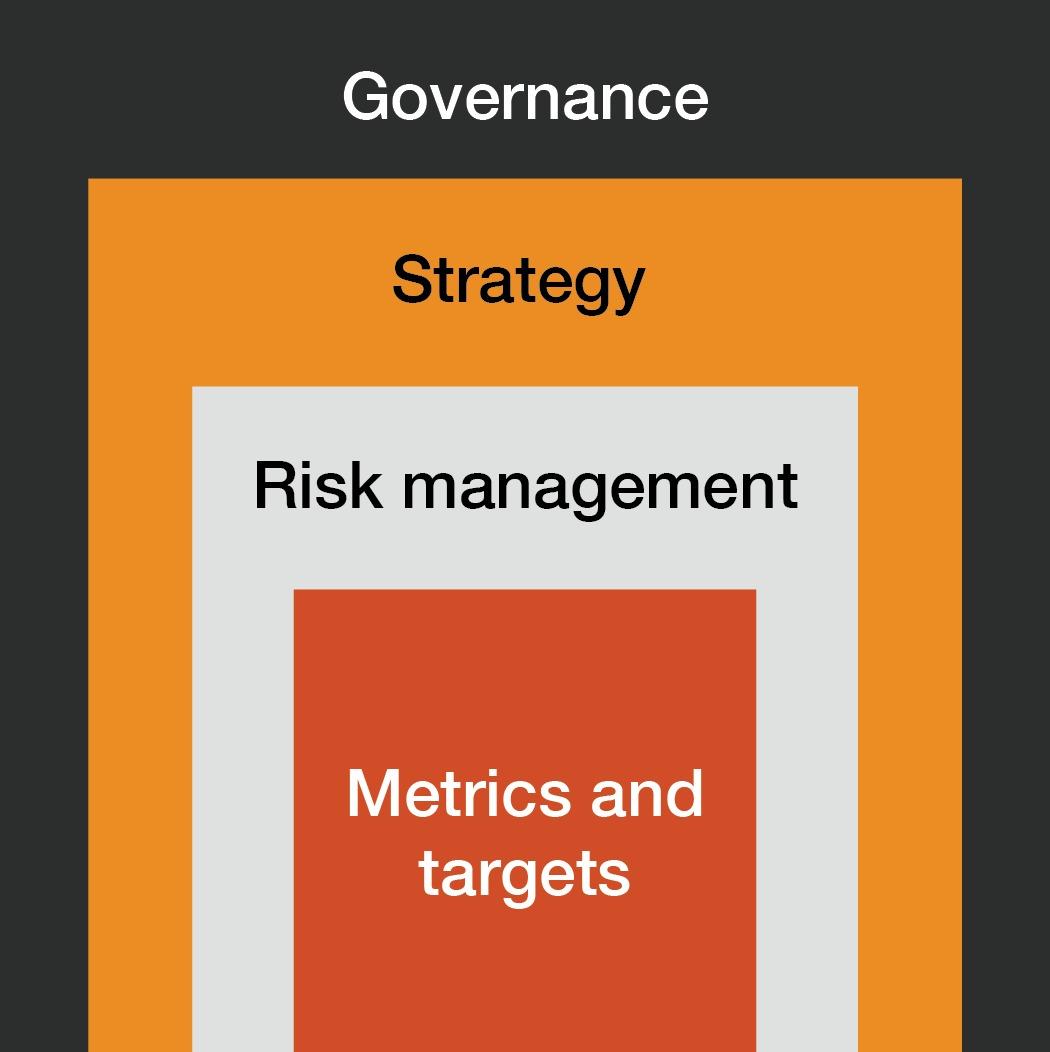

Framework at a glance

Climate-related disclosures by REs aim to provide information on relevant risks encountered and approaches adopted to address these issues. It enables different stakeholders (e.g. regulators, investors, depositors and customers) with important sources of information that can help them make informed decisions. There is a need for REs to assess and disclose their climate-related financial risks, given its growing importance and relevance.

The key thematic areas included under the climate risk financial disclosures are discussed below:

This pillar captures details relating to the governance structure of the REs for effective oversight and management of climate-related financial risks and opportunities.4 An entity is required to disclose the board and senior management’s roles in the assessment and management of the climate risks and opportunities.

This pillar focuses on the entity’s strategy in identifying climate-related financial risks and opportunities which may have material financial impact on the organisation.

This would require the entities to identify risks and opportunities over different time horizons (i.e. short-, medium- and long-term) undertake impact assessment, set targets and test the climate resilience[1] of the entity’s strategy through stress tests and scenario analysis to manage them.

This pillar focuses on procedures for recognising, evaluating and incorporating climate-related financial risks and opportunities within the overarching risk management structure. The entities are required to transparently disclose their policies and procedures for managing climate-related risks and opportunities, establish frameworks and methods for identifying and quantifying these risks, and integrate them into the existing risk management framework of the entity.

The disclosures on metrics and targets are aimed to provide information on the entity's performance vis-a-vis its climate-related financial risks and opportunities. This would include disclosure on key risk indicators (KRIs) identified, targets set against them and regular updates on progress towards achieving these targets.

Timelines

Recognising that the disclosure requirements for REs would require time to develop internal policies and reporting mechanism, the RBI has provided a staggered approach for the adoption of the guidelines, with additional time provided for disclosing data related to ‘metrics and targets’. Tier-IV UCBs are also given an additional year for the adoption of the guidelines. The implementation timeline is outlined below:

REs |

Governance, strategy and risk management | Metrics and targets |

|---|---|---|

| SCBs, AIFIs, top and upper layer NBFCs | FY 2025-26 onwards | FY 2027-28 onwards |

| Tier-IV UCBs | FY 2026-27 onwards | FY 2028-29 onwards |

The RBI rightfully recognises that the detailing of the disclosures should vary based on the size, scale and complexity of the operations of the REs. It has accordingly segregated the disclosure requirements into basic and enhanced disclosures, with enhanced disclosures being voluntary for some entities.

Key challenges in implementation

While the RBI’s draft framework is a proactive stance on climate risk, it also brings in implementation challenges for the REs. Data-related limitations (granularity, history, reliability), lack of standardised methodologies and resource constraints are few of the hurdles that entities may face in complying with the disclosure requirements. However, overcoming these challenges is essential for building resilience and fostering sustainable finance practices.

How can REs ensure compliance?

With the release of the ‘Disclosure framework for climate-related financial risks, 2024’ guidelines, the regulator has made its intention clear on compliance to climate-related disclosures. However, climate risk is an emerging risk, and different REs may be at different maturity levels in their understanding and assessment of climate-related financial risks. In our view, regulatory guidance will continue to evolve – given the diverse challenges in evolution and adoption of climate risk-related frameworks. Some key areas that entities can consider fulfilling as they embark on their climate risk management journey are listed below.

- Entities will have to work on defining the governance structure for looking at the climate-related risks and opportunities from the board and senior management levels. This would entail clearly defining the roles and responsibilities of the personnel – i.e. defining the scope and periodic reviews at all levels.

- Entities would need to develop a climate risk management policy detailing the governance structure, role of the board and senior management, detailing the internal mechanisms towards managing climate-related risks and opportunities.

- Entities must invest in upskilling/hiring of the personnel with required competencies to ensure adequate board-level governance and managerial oversight.

- Entities must start with an internal assessment of the impact of climate-related issues that they are exposed to. This may have an impact on their business model, risk appetite, portfolio composition and key financial indicators.

- Climate-based scenario analysis6 is an effective tool to run various scenarios on the entities to identify the potential risks and their impact on the entity’s strategy across different time horizons.

- Entities should develop methodologies and carry out physical7 and transition8 risk assessment on their own operations and lending portfolios.

- As part of the ICAAP, a suitable stress testing and scenario analysis methodology should be developed by the entity.

- Integrate climate risk assessment into the overall risk management framework by suitably consolidating them in the entity’s internal capital adequacy assessment process (ICAAP) and internal liquidity adequacy assessment process (ILAAP) to provide qualitative and quantitative assessment of the identified risks, their impact and mitigation plans.

- Entities must look at the various policies and processes to be set up towards managing the climate-related risks and opportunities and appropriately define the KRIs for all the related stakeholders.

- Set time-bound targets, including interim milestones, for the respective KRIs and develop internal processes to measure and report the progress towards these targets of the entity.

- Develop internal capabilities to report financed emissions for the entity.

- Develop data collection capabilities to capture appropriate data required towards internal and external reporting.

Conclusion

The RBI’s draft framework for climate risk disclosure represents a significant milestone in India’s journey towards climate resilience in the financial sector. By promoting transparency, accountability and risk management practices, the framework lays the foundation for a more resilient and sustainable financial system. The draft guidelines provide an overarching and detailed climate risk management requirement for REs, aligned with globally available disclosures standards like Task Force on Climate-related Financial Disclosures (TCFD),9 Basel Committee on Banking Supervision (BCBS)10 and IFRS S2 disclosures.11As stakeholders provide feedback and the framework evolves, collaboration between regulators, financial institutions and other stakeholders will be key to effectively address climate risk and ensure a smooth transition to a low-carbon economy.

Sources

- RBI draft disclosure framework on climate related financial risks 2024

- Discussion paper on Climate risk and sustainable finance

- Framework for acceptance of Green Deposits

- BCBS Climate-related financial risks – measurement methodologies

- IFRS Climate-related disclosures

- BCBS Climate-related financial risks – measurement methodologies

- BCBS Climate-related financial risks – measurement methodologies

- Task force on climate related financial disclosures

- Principles for the effective management and supervision of climate-related financial risks

- IFRS S2 climate related disclosures

Contact us

Associate Director, Financial Services and Treasury Risk Management, PwC India

Senior Associate, Financial Services and Treasury Risk Management, PwC India