The business of banking is changing rapidly. Products and services rendered and built on disruptive technologies are increasingly being placed in the hands of end customers, and the behaviours of banks are changing in terms of customer convenience, transparency, pricing and customer service. As costumers’ behaviours and expectations change, so do the business and operational models.

Every part of the banking value chain – from what consumers can avail and expect in terms of banking services – can now be accessed by a non-banking service provider through its technological prowess and agile and lean business models. Under these models, retail and small and medium enterprises (SME) banking services are primarily delivered through the internet or other forms of electronic channels instead of physical branches. These non-banking service providers are called neobanks and they are challenging the present status of traditional banks, by offering lower cost models and hyper-distinctive customer-centric service and experiences. Unlike their traditional counterparts, neobanks aren’t constrained by legacy systems, tightly integrated value chains, complex administrative structures and lofty regulatory requirements. Though neobanks don’t have their own bank licences in India yet, they use partners to offer bank-licensed services.

Convenience of opening and operating accounts, seamless payments, transfer and remittance solutions and alternative methods for assessing creditworthiness are some of the features that are attractive to micro and small companies and underbanked or unbanked customers such as freelancers and gig economy employees. Neobanks have provided these segments access to financial services and products, which were either scarcely available or came with heavy fees and stringent agreements.

Digital banks vs neobanks

A digital bank and a neobank aren’t quite the same, even though they appear to be based on the mobile-first approach and emphasis on digital operating models. While the terms are sometimes used mutually, digital banks are often the online-only subsidiary of an established and regulated player in the banking sector, A neobank, on the other hand, exists solely online — without any physical branches and independently or in partnership with traditional banks. This enables them to navigate and comply with the regulatory environment.

Case study

A private sector bank in India has partnered with a Fintech start-up – a neobank – to transform the employee benefits ecosystem. This neobank provides an integrated solution, comprising a multi-pocket card, a mobile app and a digital account with multiple payments wallets. Under this partnership, the private sector bank and neobank have rolled out a benefits card, which makes it easier for organisations to give employee benefits and for employees to claim them. The solution leverages state-of-the-art in-mobile technologies and has been built on the IndiaStack principles, including e-KYC by Unique Identification Authority of India (UIDAI) and Unified Payments Interface (UPI), launched by the National Payment Council of India in 2016.1

Neobanks: Fertile ground for opportunities

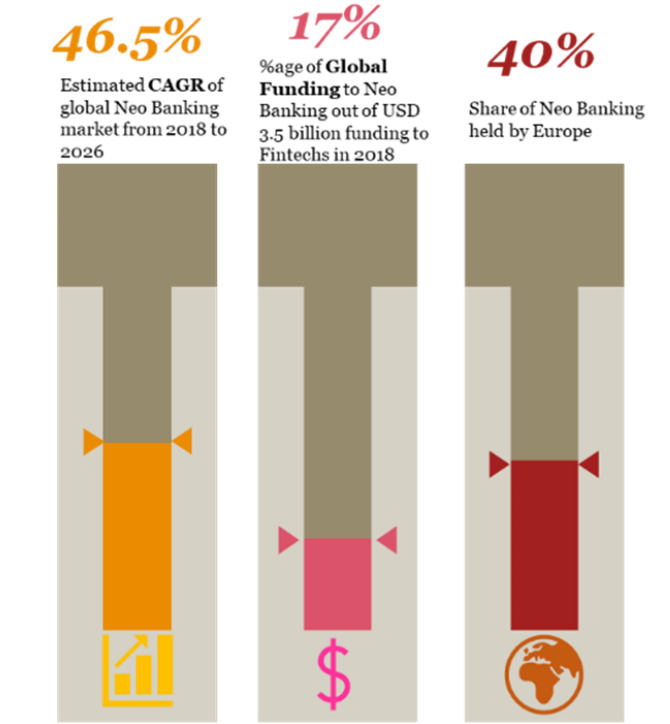

The global neobank market was worth USD 18.6 billion in 2018 and is expected to accelerate at a compounded annual growth rate (CAGR) of around 46.5% between 2019 and 2026, generating around USD 394.6 billion by 2026.2

The substantial growth potential for neobanks is driven by their low-cost model for end consumers with no or very low monthly fees on banking services such as minimum balance maintenance, deposits and withdrawals. Adoption by millennials, micro, small and medium enterprises (MSMEs), and those having sporadic incomes and earnings, embracement of innovative technologies and rising consumerism are some of the catalysts for the success for neobanks. The high adoption rates and successful business models of neobanks has piqued the interest of investors, venture capitalists and corporates, who contributed USD 586.7 million of the total funding of USD 3.49 billion received by FinTechs globally in March 2018.3

In 2018, the business sector accounted for majority of the global market revenue of neobanks4, due to growing acceptance of digital payments in both multinational companies and organisations in their nascent stages. MSMEs received services such as accounting, budgeting, taxation, analytics from neobanks at fractional costs. Such services were earlier accessible only to larger establishments, owing to the costs involved.

Pioneers of neobank adoption

As discussed above, neobanks are digital-only banks providing heightened user experiences and easy-to-integrate plug-and-play solutions for accounting, payments and tax via open application programming interfaces (APIs). But for neobanks to be adopted on a larger scale, greater penetration of smartphones and the internet is crucial, along with user comfort with digital applications and elementary knowledge of financial products and services.

Based on the above-mentioned growth and adoption factors, Europe held a substantial share – about 40%, of the global neo and challenger bank market in 2018.5 The United Kingdom is expected to lead the neo-banking market, for underlying reasons such as low concertation of branch banking as compared to other advanced economies like the US, rise of thin-file customers, overall higher financial literacy rates and the region being one of the early adopters advocacy of digital banking.

Progressing in adoption of neobanks

Asia-Pacific region is expected to witness notable growth in neobanking in future. China, India and Japan will be the fastest growing countries in the regional neobank market.6 Emerging economies like India and China are projected to exhibit healthier economic indicators in times to come based on increasing smartphone penetration, higher technological adoption, better financial awareness and an expanding number of seamless, automated, convenient and cost-efficient solutions provided by neobanks.

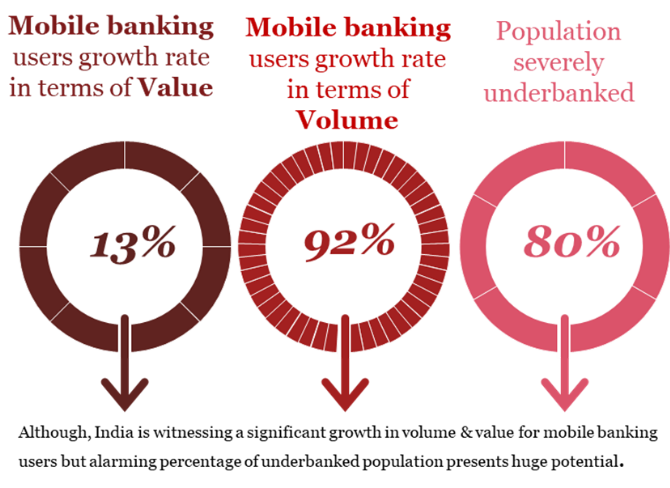

Between, 2017 and 2018, India’s mobile banking users increased by 13% and 92% in value and volume terms, respectively.7 But as per the Global Findex Database8 of 2017, 80% of India’s population remains severely underbanked, which reflects the untapped potential in the country for mobile-based neobanking services.

Neobanking in India has scope for significant growth as MSMEs in the country can avail their services on a large scale. MSMEs are numbered at 36.2 million (20179) and account for 95% of the country’s total industrial units10, but have been either out or under-served by traditional banks’ operational ambit, depriving them of formal banking and credit needs. The focus on digital economy and adoption of mobile banking, coupled with the underserved banking, financial and credit needs of both MSMEs and retail segments, present substantial market opportunities for neobanks in India.

At present, there are four main neobanks in India, which have received sizeable funding from investors.11 In addition, there are global banks, which view India as an engine of growth. Recently, one of Singapore’s largest banks launched its services in India, including savings accounts, fixed accounts, payments solutions, transfers and investment management. The services offered by the bank are completely digital, without any presence of physical branches.

Advantages and shortcomings of neobanks

Advantages of neobanks over traditional banks for MSMEs

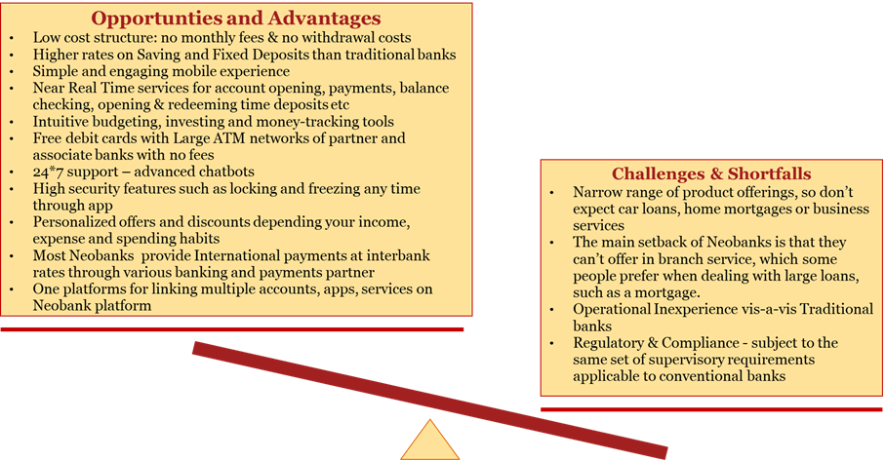

- Customer experience: neobanks don’t offer novel banking services. Their services are similar to those of traditional banks, but with a hyper-enhanced and personalised customer experience. Neobanks have significantly leaner business models and superior technologies at their disposal compared to traditional banks, providing ease and efficacy in services, such as seamless account creation, round-the-clock customer service supported by chatbots, near real-time cross-border payments, and artificial intelligence (AI) and machine learning (ML)-enabled automated accounting, budgeting and treasury services.

- Automated services: Apart from providing primary banking services, neobanks offer automated and near real-time accounting and reconciliation services for bookkeeping, balance sheets, profit and loss statements and taxation services such as GST-compliant invoicing, tax payments record keeping and reconciliation, on mobile platforms for affordable costs..

- Transparency: Neobanks are transparent and strive to provide real-time notifications and explanations of any charges and penalties incurred by the customer.

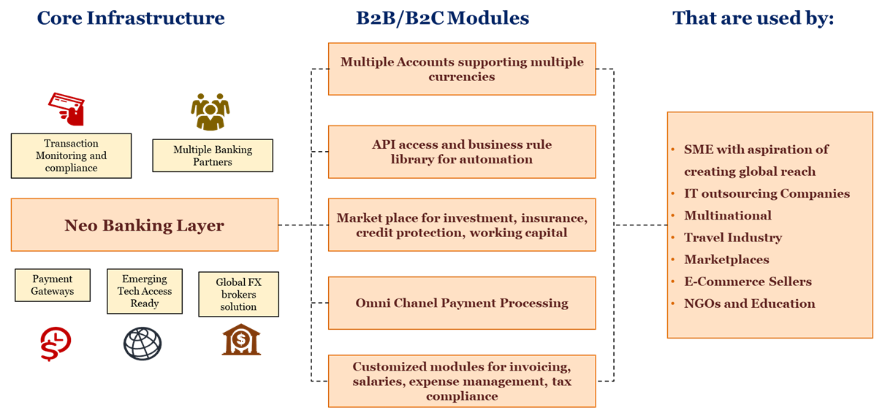

- Easy-to-use APIs: Most neobanks provide easy-to-deploy and operate APIs to integrate banking into the accounting and payment infrastructure.

- Deep insights: Most neobanks provide dashboard solutions with highly enhanced interfaces and easy to understand and valuable insights for services such as payments, payables and receivables, and bank statements. It’s beneficial for businesses with significant expenditure and appropriate number of employees, to be provided with such insights, reduce expenditure and boost productivity and revenue.

Case study

In India, a neobank is catering its services and solutions for SMEs and playing a leading role in aiding small businesses in managing their finances conveniently and comprehensively. The neobank provides a platform that helps such businesses send and receive payments, automate their accounting and reconciliation, generate and track compliance of invoices with direct and indirect tax laws, and access third-party banking and business applications from its platform, allowing multiple businesses to simultaneously manage all their banking needs under a single platform.

Regulatory considerations for neobanks in India

In India, virtual banking licences are still not granted, though there are foreign national banks offering digital-only products through their Indian subsidiaries. The Reserve Bank of India (RBI) remains stern in prioritising banks’ physical presence, and lately reinforced the requirement for digital banking service providers to have some physical presence12.

The significance of brick-and-mortar bank branches is to serve customers and redress their disputes and grievances in person. In its 2014 Guidelines for Licensing of Payments Banks, the RBI had highlighted that it does not see payment banks becoming '"virtual" or branchless banks.13

Presently, neobanks in India are addressing the regulatory predicament by outsourcing their banking responsibilities to those with licences, creating strategic partnerships with traditional banks and providing amplified services on behalf of existing ones. This model is already being used worldwide by some of the biggest names in neobanking.

As part of their business strategy and to overcome regulatory hindrances, neobanks partner with traditional banks and offer business and consumer banking services. For the end customer, financial and banking services are offered by the neobank, but from a regulatory perspective, monetary transactions are managed by their partner banks.

Road ahead

Attributes and offerings like accessibility, cost-effective multiple banking and financial functionalities under one umbrella, and personalisation are some of the driving factors for neobanks globally. Secondly, FinTechs are building niche solutions focusing on blue-collar workers and the underserved needs of thin-file MSMEs, which is the way forward.

Neobanking can work as an extension of measures undertaken to solve the challenges of financial inclusion and bundling banking services with other financial services—for example, services like opening of bank accounts for immigrants, facilitated through new onboarding procedures not based on traditional documentation of identification. With narrow targets initially, neobanks could expand by adding more functionalities and services over time.

Although digital and neobanks are gathering momentum, most are yet to show sustained profitability.14 Nevertheless, they have great potential to be disruptors in banking and financial services, and the key towards becoming profitable entities would be to convince traditional banks to invest in new-age technology and re-engineer processes to provide seamless and swift customer experiences.

With competition mounting among traditional banks, new-age FinTechs, technology firms and non-banking entrants, it is yet to be seen whether the market is deep enough for neobanks to grow sustainably and equitably. How neobanks manage vital impediments in terms of regulation and compliance, data and cyber security, seamless API integration and expansion of products and services will be the fundamental determinants of their success.

With inputs from Raghav Aggarwal and Avneesh Singh Narang

Sources:

1Case Study sourced from https://www.financialexpress.com/industry/banking-finance/yes-bank-partners-fintech-startup-niyo-eyes-5-million-customers-in-5-years/383055/

3https://gomedici.com/march-2018-fintech-funding-lending-neo-banks-topped-charts

9https://www.statista.com/statistics/718232/india-number-of-msmes-by-type/

10https://www.ibef.org/download/SMEs-Role-in-Indian-Manufacturing.pdf

12https://m.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=892

13https://www.rbi.org.in/scripts/PublicationsView.aspx?Id=18061

14https://qz.com/1679197/when-will-digital-banks-like-n26-and-revolut-start-making-money/

Contact us

Vivek Belgavi

Partner, Financial Services - Technology and FinTech Leader, PwC India

Tel: +91 22 6669 1734