The evolving landscape of cross-border payments

July 2021

Cross-border payments: Market overview

With global economies becoming increasingly connected, there is growing demand for a fast, secure and efficient cross-border payments system. As per a recent report,1 81% of cross-border payment transactions involved money being sent to support friends and families abroad. There has been a recent surge in international remittances, with an increase of 61% over the last 12 months.2

Cross-border payments landscape

The cross-border payments ecosystem includes B2B, B2P, P2B and P2P merchants. Processing of cross-border remittances takes place through various legacy channels such as SWIFT/correspondent banking, post, Rupee Drawing Arrangement (RDA) and Money Transfer Service Scheme (MTSS).

Despite the availability of conventional modes, transaction fees and excessive regulatory and documentation requirements make small-value transactions unattractive. The cost and speed of delivery strongly influence the customer’s final selection of payment mode. Recently, FinTechs have leveraged technology and captured the white space in cross-border payments left unaddressed by legacy models.

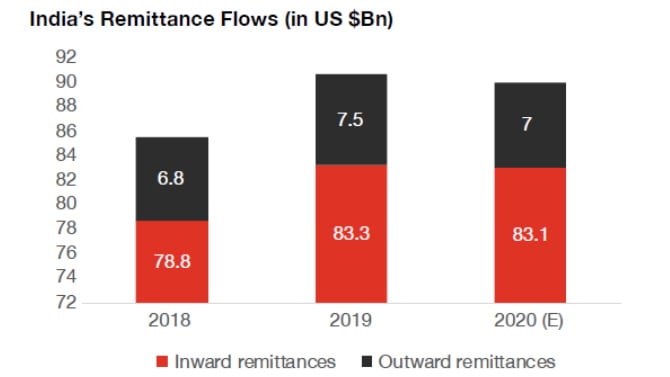

At around USD 83 billion, India is the largest global market for inward remittance flow, followed by China and Mexico.3 India’s inward remittances primarily come from the Middle East and the USA, with the majority of outward remittances sent to Nepal and Bangladesh. Since 2016, India’s cross-border remittances have been growing steadily at a CAGR of 8%,4 driven by the increase in global mobility of goods and services, international travel and international workforce.

India’s Remittance Flows (in US $Bn)

Source: World Bank

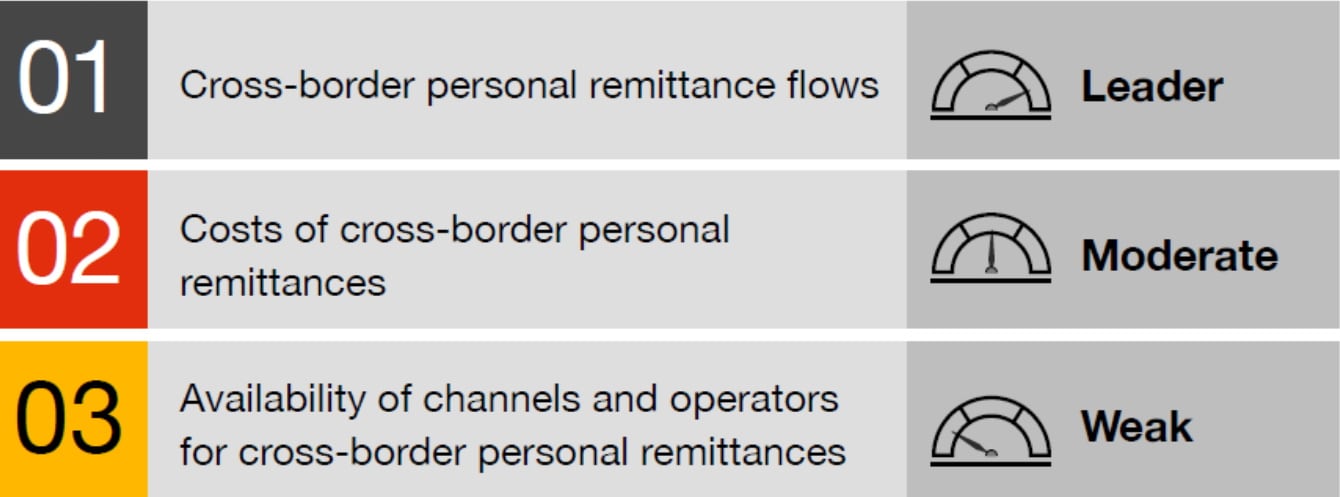

The Reserve Bank of India (RBI) recently highlighted how Indian crossborder payments compare against international competitors.

Source: RBI

Cross-border remittance options

Some of the prominent modes of remittance and cross-border transfer are as follows:

Cross-border remittance models

Past/current

- Correspondent bank/money

- Money transfer service scheme (MTSS)

- Rupee Drawing Arrangement (RDA)

- Postal channels

New current

- Emergence of FinTechs

Future

- Faster payment rails

- Distributed ledger technology (DLT)

a) Correspondent bank/SWIFT

Banks and other financial institutions use SWIFT extensively to send and receive international payments. The SWIFT network comprises over 11,000 financial institutions across over 200 countries. SWIFT is being used by banks, securities dealers, asset management companies, clearing houses, depositories, exchanges, etc.

Indian banks tie up with foreign correspondent banks and open a NOSTRO account. The correspondent and Indian bank process the transfer request through the SWIFT messaging infrastructure.

Transactions take one to five days to credit and charges depend on the amount and country (a few Indian banks have a flat fee structure starting at INR 500). While institutions and individuals across geographies have adopted SWIFT widely for cross-border payments, the pace of remittance is a concern given the emergence of faster payment rails.

b) MTSS5

MTSS is a strategic tie-up between overseas principals and Indian agents who disburse funds to beneficiaries in India at ongoing exchange rates. Transfers usually take one to three days with charges ranging from 0.3–5% of the transaction amount.

This service can only be used for inward personal remittances with a maximum transaction limit of USD 2,500 and a maximum of 30 transactions per beneficiary per year. Trade-related remittances (remittances towards the purchase of property, etc.) are prohibited under this arrangement.

c) RDA

Indian banks have partnered with various international exchange houses to provide a faster remittance facility to Indians residing outside the country. AD-1 banks6 tie up with non-resident exchange houses to maintain vostro accounts in FATF-compliant countries.7 Customers can use these exchange houses to send money to India. The money is credited to the beneficiary account held with the bank maintaining the RDA within a few hours.

RDA only facilitates inward remittances. There are transaction limitations (value or volume) for individual transactions. There is an transaction cap of INR 15 lakh for trade-related transactions.

d) Postal channels

The International Financial System (IFS) is a software/platform developed by the Universal Postal Union (UPU) to facilitate both inward and outward remittances through the postal channel across partner countries. These transfers are conducted over electronic data interchange (EDI) messages from India Post’s central server to the IFS national server to the destination country postal operator through the UPU system.

This service is provided through the post office in India and operates through the La Poste Group in France and the IFS in the UAE using international money orders. There are two primary services, normal and urgent, with delivery times ranging from two to five days. Commercial transactions such as investments, loans, donations to charitable institutions, trusts or non-resident external (NRE) accounts are prohibited.

e) Emergence of FinTechs

FinTechs have leveraged technology to introduce low-cost solutions for international payments for individuals, small businesses and corporates. FinTechs have revolutionised the cross-border payments ecosystem through enhanced customer service, extensive global reach, flexible payment options, lower fees, and reduced transaction times.

FinTech companies facilitate transfers in a secure, fast and affordable way. There are two primary models:

- cross-border payment rails that don’t run on traditional bank networks

- technology solutions that allow clients to connect to legacy bank rails more easily.

In this model, a FinTech company has a network of accounts across several countries maintaining balances in the local currency with a treasury team responsible for management of these local accounts.

The customer initiates a transaction at the local FinTech office in the local currency. The transaction details are passed on to the office in country B which pays the agreed amount of money in the local currency to the beneficiary’s domestic account.

Each cross-border transaction consists of a set of two individual domestic transactions. Settlement between accounts/offices is done several times a month to optimise exchange rates. The transfer fees range from 0.25–3% of the transaction amount and depend on the destination.

f) Future models

Faster payment rails

FinTechs are leveraging entrenched faster payment rails to offer seamless cross-border payment services. The transactions will be funded through the user’s bank account or registered card. Integration of UPI with the faster payment systems of Singapore and Thailand, which uses proxy identifiers like mobile numbers, will enable payments through this route. This would reduce the information and effort required for cross-border payments. The partnership will help FinTech companies to expand their presence in several markets and more aggressively compete with rivals that have a wider reach.

Distributed ledger technology (DLT)

FinTechs, banks and IT & ITeS companies have been experimenting with DLT in the cross-border remittance space. This model uses a bidirectional messaging and settlement component that validates transactions using DLT before funds are transferred.8 This model is gaining increasing acceptance among customers who transfer smaller amounts of money, particularly in small-to-medium businesses.

Key challenges

Cross-border payments involve different time zones and different currencies. Multiple compliance checks add layers of friction such as significant delays, exorbitant charges and uncertain receipt of payment.

Innovation and partnership among stakeholders can help in addressing challenges around speed, cost and transparency in cross-border payments.

Cost

The charges for cross-border payments vary depending on the transaction amount, payment method, transfer destination, and exchange rates, which may vary across markets and service providers. Usually, the charges stand at anywhere between 0.3–20% of the transaction amount. At times, the cost for the provider increases due to the complexity or management of settlement in multiple currencies. Factors contributing to high costs include the process for ensuring KYC/AMC guidelines and partnerships. Standardised regulation and innovative technologies could reduce these costs and reduce the overall transaction costs for customers.

Speed

Many countries have enabled domestic real-time payments. However, cross-border payments take a considerable amount of time due to various checks and controls, as well as multiple layers. The most common reasons for delay are incomplete remittance information and anti-money laundering and fraud checks. Institutions have different processes to mitigate risks. Digitalisation and standardisation information sharing across borders can help in faster payment processing.

Lack of standard regulations

Cross-border payments are subject to the regulatory requirements of the origin country, the destination country and any other jurisdictions they pass through on the way. Each country has its systems and regulatory authorities to protect consumers and their personal data and avoid fraud and illegal activities.

In India, the RBI regulates and issues guidelines for cross-border payments with respect to AML, KYC, limits, etc. In Singapore, the MAS oversees cross-border payments. In Europe, they use the SEPA system and other legislation like PSD2.

Besides, banks have specific and high-level regulatory and compliance requirements for AML and KYC. This may increase the cost for setting up the process, though the cross-border payment volumes may not justify the incurred compliance cost. Standardisation of the AML and KYC process would help in creating a level-playing field.

Message format

Standardisation and interoperability are important to increase the efficiency and scale of cross-border retail payments. The largest number of crossborder payments are processed using the SWIFT MT103 messaging format, which is highly reliable but rather limited in terms of the amount of information it can carry. Any information that cannot be captured through MT103 and MT199 is usually sent in an accompanying email. There are a few payments systems that use their own proprietary format while there are some systems that follow ISO 8583 messaging related to card payments.

One of the biggest challenges in improving the speed of cross-border payments is interoperability. The main advantage of instant or faster payments is the reduction of transaction time. Without system and message compatibility, any payments made between systems would require translation, which is time intensive and increases the transaction risk due to the higher possibility of errors. The introduction of ISO 20022 is a step towards mitigating this problem, with many countries adopting or planning to adopt these messaging standards. While converting to ISO 20022 can bring in interoperability and data richness, it is a long-term solution as the process is time and effort intensive. Therefore, there will be a delay in achieving standardised global messaging formats but that would not be a major obstacle in the development an evolved cross-border payments system.

Customer experience differs by geography

Another challenge in cross-border payments is people and cultural challenges. Customer experience varies across countries – it may be important in one country but less of a priority in another. Hence, operators serving in this space should consider cultural differences of the operating country and deliver solutions accordingly. Several FinTechs have tried to enhance their customer experience by offering services in multiple languages and increasing the appeal of their services in multilingual countries.

Speeding up cross-border payments

There are several systems that facilitate faster cross-border payments in both Europe and Asia, and uniquely address related challenges.

Europe

The SEPA Instant Credit Transfer (SCT Inst) system provides instant payments facilities in over 20 countries. All transactions done through SCT Inst are in euros, thereby making it a unique example of a single-currency cross-border payments system. The figure below highlights some of SCT Inst’s key features:

Source: PwC analysis

The Nordic countries of Sweden, Denmark and Finland are set to launch their own faster cross-border payments system in mid-2021. The P27 Nordic Payments system would be the first multi-currency, multi-country system supporting the Swedish krona and Danish krone along with the euro.

Asia

The development of an all new real-time payments system is not always a feasible option. Countries with existing faster payments systems have been exploring the opportunity of linking them with similar systems in other countries to facilitate cross-border payments. This has been successfully implemented by the Monetary Authority of Singapore (MAS) and the Bank of Thailand (BoT) who linked their retail faster payments systems PayNow and PromptPay,9 in April 2021. This is the first global instance of two retail faster-payments systems being linked, facilitating instant cross-border retail payments. Customers in both the countries can engage in low-value retail transactions using their linked mobile numbers and internet banking. The figure below highlights some of the key features of the collaboration between PayNow and PromptPay:

Source: PwC analysis

This partnership has helped in reducing transaction times to a few minutes from one‒two business days. The participants have entered into agreements to keep the pricing aligned with market standards and benchmark forex with the prevailing rates.

The above-mentioned payments systems in Europe and Asia have been developed to address the issue of cross-border payments across a specified region or between countries. There are several limitations to these systems, including:

- Limited reach: These are not universal cross-border payments systems and restricted to a limited number of countries.

- Currencies: These systems can support only a limited number of currencies.

- Transaction limits: There are significant limitations on the usability of the system for business or large-value transactions due to low transaction limits.

Other payments systems like India’s UPI can replicate the above-mentioned examples and enhance cross-border payments offerings.

The impact of UPI

UPI is in a prime position to be leveraged for enhancing cross-border payments services. UPI’s domestic success has been internationally recognised and several countries have attempted to recreate the same.

The impact of UPI on cross-border payments is expected to be significant and similar to the impact of UPI on the domestic payments ecosystem.

Advantages of UPI for cross-border payments

UPI offers 24x7 services to domestic customers and would address significant pain points if extended to cross-border payments. Traditional cross-border payments methods are restricted to banking days and hours. Though the digital models offered by FinTechs have been helpful to some extent, they are still limited by bank timings.

UPI would allow users to make cross-border payments at any time through multiple digital channels.

UPI is an instant payments system that completes and settles transactions in near real time. The transaction times in current cross-border payments services range from a few hours to overnight and longer. UPI has the potential to significantly reduce transaction times and associated risks.

Using proxy identifiers for payments is one of UPI’s major advantages. This makes transactions significantly easier as only the linked mobile number is required.

The partnership between the faster payments systems of Singapore and Thailand prove that it is less cumbersome to set up cross-border payments systems using proxy identifiers like mobile numbers.

UPI should be able to reduce the transaction charges associated with cross-border payments as local taxes, cross-border fees and exchange rate fluctuations would not impact the overall costs.

UPI could also help in reducing the bank fees for cross-border transactions which account for the largest component of border-payments costs. The payments interface would simplify the corresponding relationships between international banks and reduce the time and effort required for each transaction, thereby allowing banks to charge a lower transaction fee.

Challenges in the global adoption of UPI

UPI could also have several limitations as a cross-border payments system. Some of these limitations are:

Transaction limits

UPI currently has a cap of INR 1 lakh on most domestic transactions and a higher cap of INR 2 lakh on select transactions like capital market investments, bill collections and insurance payments. The lower limit has restricted UPI’s appeal for larger value/business-to-business (B2B) payments. The payments limits in UPI would require reconsideration as cross-border payments tend to have larger ticket sizes due to exchange rates. For example, a US-based financial services company that currently offers inward remittances using UPI is still confined to the domestic limit of INR 1 lakh. The expected increase in limit across transaction types could work towards addressing this to some extent, but unique limits for cross-border payments using UPI may be more beneficial.

Individual partnerships

The National Payments Corporation of India (NPCI) would be required to enter into multiple partnerships to expand the reach of UPI.

Transaction disputes

Transaction-related disputes would be difficult and complicated to settle due to immediate completion of payments with foreign-exchange considerations.

Implementation opportunities

There are several ways UPI can be introduced in the cross-border payments ecosystem.

1. Partnerships

The partnership between PromptPay and PayNow could be considered as the blueprint for future collaborations between retail payments systems. The NPCI can explore the opportunities to partner with other existing faster payments systems to facilitate cross-border payments. There are several factors to consider when exploring partnership opportunities, including:

- Reason for partnership ‒ large remittance market/popular tourist destination

- Statistical evidence ‒ significant transaction volumes with growth potential

- Reputation, stability and security ‒ political and financial stability of partner (ensure minimum transaction risk)

- Infrastructure interoperability ‒ minimise integration challenges due to the lack of infrastructure compatibility

Source: PwC analysis

India is one of the largest markets for inward remittances and it could collaborate with several potential partner countries which account for large transaction volumes.

India has already initiated a partnership with Singapore for using BHIM UPI for QR code payments. Static QR code payments require customers to enter the amount in Singapore dollars which is then converted into INR by the app. It also accepts dynamic QR code payments by displaying the amount for customer approval in both the currencies.

2. Establishment of a UPI-based cross-border remittance network

The NPCI has been working on expanding the acceptance of UPI through its subsidiary NPCI International. It aims to increase UPI’s international footprint and popularise products such as RuPay. It is also providing technological assistance through licensing and consulting to help other countries build their faster payments systems. It has partnered with Singapore’s Network for Electronic Transfers (NETS) to enable Indian travellers in Singapore pay through BHIM UPI by scanning QR codes at NETS terminals. This collaboration provides an additional payment mode facilitating trade-related cross-border small-value payments.

This could potentially be the first step in creating a multi-country payments infrastructure that would connect several countries with faster payments/ remittance systems based on UPI’s structure and standards. Any integration of these systems would be significantly easier due to the use of UPI’s framework.

The role of FinTechs

The NPCI has increased its global reach by expanding UPI’s usage internationally.

A US-based financial services company recently introduced a new inward payment method that allows users to send money to India using only the beneficiary’s UPI ID rather than a mobile number or bank account details. This is a significant first step in leveraging UPI for faster inward remittances and cross-border payments. The company’s infrastructure allows its customers to avail this service in over 200 countries. It has also tied up with a digital wallet platform to provide inward remittance services to India from the US, allowing customers to send up to INR 1 lakh through the app. UPI will help in facilitating the transaction’s final step (from the recipient bank to the beneficiary) and provide a cash pick up option as well.

Other international FinTechs are also looking to expand their remittance services to India. A US-based online payments company has integrated with UPI to offer remittance services using only the beneficiary’s UPI ID. This is the most efficient and short-term method of cross-border payments using UPI.

FinTechs have managed to reduce domestic transaction charges and they could be instrumental in decreasing cross-border payments costs as well. Stronger digital identification (using the Aadhar system) and robust antimoney laundering (AML) and risk assessment capabilities give FinTechs the potential to support more affordable and remotely accessible cross-border banking services.

Conclusion

UPI’s existing infrastructure could be highly beneficial for cross-border payments. Instant payments through UPI would facilitate a much simpler and more efficient transaction process in India, one of the largest inward remittance markets. UPI could have a significant impact on the current methods used for cross-border remittances. It could also be used in other countries in partnership with faster payments systems.

| Abbreviation | Full form |

|---|---|

| FATF | Financial Action Task Force |

| MAS | Monetary Authority of Singapore |

| MTSS | Money Transfer Service Scheme |

| PSD2 | Payment Service Directive 2 |

| SEPA | Single Euro Payments Area |

With input from Aarushi Jain, Siddharth Gupta, Kanishk Sarkar, Anand Jeyachandran and Tushar Gupta.

Sources

- Borderless payments

- India received $83 billion in remittances in 2020: World Bank report

- The Indian payments handbook – 2020–2025

- Background paper on remittances from the gcc to india: trends, challenges and way forward

- Banks with an RBI licence to buy and sell foreign exchange for specified purposes

- What is rupee drawing arrangement (rda)?

- Impact on real-time cross-border payments

- Singapore and thailand launch world's first linkage of real-time payment systems

Payments technology updates

Paytm Payments Bank to enable international remittances

Times of India

Paytm Payments Bank (PPB) plans to expand into facilitating cross-border as well as domestic remittances. The bank’s CEO said that the new umbrella entity (NUE), proposed by PPB and other investors, will change the pace of digital payments in the country, if approved.

RBI steps in to push UPI, RuPay’s global reach

Financial Express

The Reserve Bank of India (RBI), in close collaboration with the government and National Payments Corporation of India (NPCI), is working to expand the reach of Unified Payments Interface (UPI) and RuPay globally.

RBI announces 2nd cohort under regulatory sandbox with theme of 'cross border payments'

Money Control

The Reserve Bank on Wednesday announced the second cohort under the Regulatory Sandbox (RS) with the theme of 'Cross Border Payments' and also reduced net-worth requirement for entities interested in participating.

Can fintech be the catalyst in revolutionising cross-border banking in India?

CNBC 18

Armed with agility, state-of-the-art technology and a modern outlook, fintech is shifting the way cross-border banking services are consumed while providing a delightful user experience.

Google Pay Now Lets Users Send Money From US to India and Singapore

NDTV

Google is planning to expand foreign transfers by the end of the year to more than 200 countries and territories through Western Union, and to more than 80 countries through Wise.

As Real-Time Payment Rails Rise, Interoperability Comes Into Focus

PYMNTS

Embracing new payment rails, and enhancing the value of existing ones, remains a key part of promoting overall payment innovation.

PayPal's Xoom Adds Real-Time Payments For Remittances To India

PYMNTS

PayPal's Xoom, an international money transfer service, has integrated with NPIL's/NPCI's Unified Payments Interface (UPI) to offer inter-bank transactions in India

Contact us