Digital payment opportunities in emerging markets

March 2019

Emerging markets landscape

The burgeoning digital payments industry has scaled up rapidly over the last few years across South Asia. The rise of affordable smartphones and subsequent Internet and mobile penetration have led to significant growth in the digital payments space. According to research conducted by Forex Bonuses,1 Canada tops the list of most cashless countries in the world, followed by Sweden (only 2% cash transactions2), the UK, Australia and a few leading Asian countries. The people in these mature markets are aware of digital payments and have steadily embraced non-cash methods over the years.

Emerging markets in South Asia, on the other hand, are witnessing a slow transition from a cash-driven to a digital payments society. Governments and regulators in South Asian emerging markets like Bangladesh, Nepal and Sri Lanka have a clearly defined roadmap for digital transformation and encouraging citizens to go ‘less cash’. The current usage of cash in these countries exceeds 90%.3 Nevertheless, they have seen some traction in the last few years, primarily due to mobile and Internet penetration and a focus on financial inclusion through mobile-based services.

Mobile financial services (MFS) targeted at the underbanked and unbanked population are a huge success and they now account for a majority of digital transactions in Bangladesh by volume. Nepal is heavily dependent on inward remittances, which amount to as much as 30%4 of the GDP. Smartphone-based mobile money services are slowly gaining momentum as part of the payments ecosystem. However, debit cards dominate the plastic card market, and the recent association with international payment networks for QR-based payments has paved the way for players to offer new solutions in this space. In Sri Lanka, more than 80% of adults have access to financial services.

Regulators and governments of emerging countries can set up a separate entity like the National Payments Corporation of India (NPCI) to promote retail payments. Moreover, a truly open domestic cards scheme like RuPay in India or UnionPay in China may be set up to expand the digital payments ecosystem.

| Bangladesh | Nepal | Sri Lanka | |

|---|---|---|---|

| Population | ~ 166 million | ~30 million | ~21 million |

| Mobile/Internet | ~94% mobile penetration ~55% Internet users |

~130% mobile penetration ~57% Internet users |

~130% mobile penetration ~32% Internet users |

| Cards* | ~13 million cards | ~6 million cards | ~22 million |

| ATMs | 1 ATM per ~16,500 people | 1 ATM per ~9,500 people | 1 ATM per ~5,000 people |

| POS | 1 POS per ~3,800 people | 1 POS per ~2,500 people | 1 POS per ~400 people |

| Participants | Bangladesh Bank, banks, MFS, wallets players, national payments switch | Nepal Rastra Bank, banks, digital wallets, mobile network operators, SCT, card schemes | CBSL, banks, mobile payment services, card schemes, LankaClear |

| Instruments | Cards, digital wallets, QR code payments, mobile money/QR code payments, NFC payments | Cards, digital wallets, QR code payments, mobile money/QR code payments, NFC payments | Cards, wallets, JustPay, LANKAQR, mobile payment services/real-time payments, QR code payments |

Key policy/regulatory initiatives

Bangladesh

Government initiatives: Access to Information (a2i) is a programme jointly run by the government (Department of IT) and Bangladesh Bank. They also jointly initiated the Digital Financial Service (DFS) Lab+ to increase digital payments. The objective of the initiative is to understand the challenges being faced by the unbanked and underserved segment and address the same through citizen-centric innovative products and services and financial literacy.

2FA Relaxation for contactless credit card payments: The Central Bank of Bangladesh has relaxed the second-factor authentication (2FA) for NFC transactions made through credit cards. The transaction limit has been set as BDT 3,000 per transaction. This has encouraged card schemes to partner with multiple banks to expand contactless offerings.

Regulatory initiatives: Bangladesh Bank is in the process of setting up a regulatory sandbox, rolling out a centralised QR and setting of digital transactions targets to various ministries. This move will change the digital payments landscape and bring Bangladesh on par with neighbouring emerging markets.

Nepal

Nepal Rastra Bank (NRB) sets transaction limits: The NRB has set an upper cap per transaction along with daily and monthly limits for digital payment instruments/channels like debit card withdrawals and prepaid card/wallet loading. It also reduced the credit card cash withdrawal limit to 25% of the credit limit, which will boost digital payment transactions. Thus, clarity has been provided on the regulations around various payments offerings.

Regulatory framework for telecom companies to provide payment services: Traditionally, mobile payment initiatives followed a bank-led model. However, in 2016, NRB opened the door for telecoms to operate mobile payment services by setting up by a subsidiary firm. This Central Bank policy enables leading telecom operators to enter into the digital wallets business by obtaining a payment service operator/payment service provider licence.

Sri Lanka

Mobile Payments Guidelines No. 1 and 2: When mobile money services were initially introduced, the Central Bank of Sri Lanka (CBSL) required all users to have a bank account. When the uptake of these services was observed to be low, the CBSL revised its regulations in 2011 and released ‘Mobile Payments Guidelines No. 1 of 2011 for the Bank-led Mobile Payment Services’ and ‘Mobile Payments Guidelines No. 2 of 2011 for Custodian Account Based Mobile Payment Services’. The revised regulations allowed customers to register for mobile money accounts without a bank account and helped a leading mobile money service provider increase its registered user base to 1 million in one year for in 2012.5

National QR code standards (LANKAQR): In October 2018, the CBSL specified a set of guidelines that need to be adhered to by licensed banks, licensed finance companies and licensed operators of mobile phone-based e-money systems while offering QR code payments. These guidelines also specified that all LANKAQR payments would be charge-free for consumers and a market-determined merchant discount rate (MDR) would be applicable for merchants. This will encourage usage of new and convenient payment channels and thus enhance the user experience. In addition, it boost digital transactions in offline kirana stores.

Roadmap 2019 by CBSL: In its roadmap for monetary and financial policies for 2019, the CBSL has highlighted that in order to promote digital payment initiatives, it will facilitate the implementation of the ‘National Transit Card and Infrastructure Framework’ for ticketing and fare collection. With this objective in mind, it has introduced a nationally accepted transit card which can be used for bus and rail transport in Sri Lanka. This is expected to reduce the use of cash at various transit points.

Key challenges

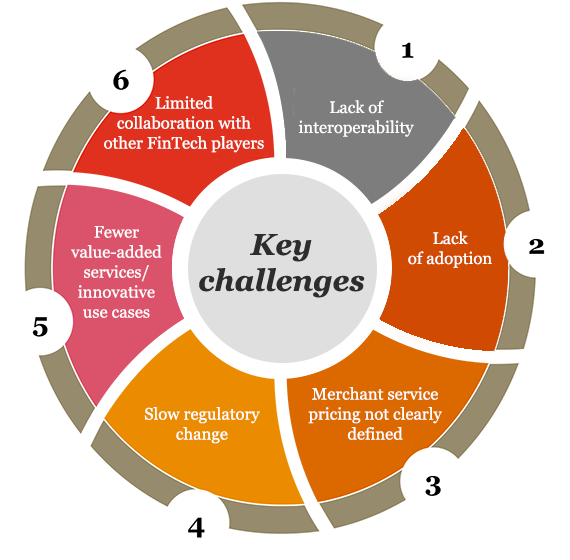

The payments industry has grown increasingly complex and fragmented over the last few years. However, there are a few challenges that must be addressed to create a thriving digital payments in these countries.

Lack of interoperability: Today, enabling interoperability is key for emerging digital payments offerings. In all the countries mentioned, customers are required to have multiple wallets for purchase transactions. This hinders existing wallet users from using these services at merchants where another wallet is accepted.

Lack of adoption: As mentioned before, the uptake of digital payments has been slow in these countries. For example, digital payments still comprise only about 5% of total transactions in Sri Lanka.4 In addition, low investment in acceptance infrastructure by financial service providers has contributed to low awareness and, consequently, low adoption of digital payment instruments.

Merchant service pricing not clearly defined: For certain payment instruments, merchant service pricing is not capped. In all the three countries, the acquiring bank/digital wallet providers levy charges ranging from around 1–4%. While large business set-ups can absorb this cost, small businesses with low profit margins tend to pass on the commission cost to consumers. This, in turn, puts a burden on the merchant and reduces the incentive to use cards at the PoS.

Slow regulatory change: While some changes have been made in the recent past to facilitate mobile money transactions and QR transactions, other regulations still hinder the uptake of mobile payment services. These include low wallet limits which obstruct use cases like remittances and business-to-business (B2B) and business-to-consumer (B2C) payments like disbursements. Lack of awareness about the regulatory framework along with low clarity on licensing and regulations for non-bank players issuing cards and wallets also affects the uptake of these instruments by merchants and other service providers.

Fewer value-added services/innovative use cases: The mobile financial services/wallets of these countries have a greater focus on standard services like mobile recharge, utility bill payment and fund transfer. Service providers can look at innovative use cases by offering unexplored financial services on their platform and introducing rewards/loyalty programmes.

Limited collaboration with other FinTech players: FinTechs can play a vital role in building solutions to reach the unbanked population in emerging countries. Currently, very few payment players/banks are collaborating with FinTech companies to launch new/diversified offerings.

The way ahead

In emerging countries like Nepal, Sri Lanka and Bangladesh, since payments are still at a nascent stage, a large number of opportunities are available in relatively untapped business segments. Some of the opportunities which are likely to grow in future in these markets are discussed below:

Contactless payments: While contactless cards have already been launched in Bangladesh by a major payment network, the technology is yet to be explored in Nepal and Sri Lanka. Top management of card companies in Sri Lanka has expressed the need for accessible payment modes like contactless cards in the industry. In Bangladesh, major card networks are looking to tie up with banking partners for the issuance of contactless cards. In addition, there is considerable scope for setting up infrastructure for these cards and payment players can look at tapping this opportunity.

Charting out digitisation roadmaps: Payment bodies in Nepal, Bangladesh and Sri Lanka need to devise a digitisation roadmap for payments. This should include strengthening acceptance infrastructure, promoting and incentivising digital payments for the right target audience, and partnering with key technology players. Most importantly, it should outline the role of specific regulatory bodies in monitoring, regulating and promoting digital payments.

Strategic partnerships: Partnerships with FinTechs play a crucial role in the development of a digital payments ecosystem by promoting innovation and enabling open loop payments that promote the adoption of digital payments.

In Sri Lanka, such partnerships have already set the ball rolling with the introduction of a QR code for low-value payments, contactless payments and payment gateways for processing m-commerce transactions through tokenisation. In Bangladesh, increased remittance partnerships with international players have opened up the market for more such partnerships with money transfer companies to enable digital remittance transfers to accounts and wallets in Bangladesh. Thus, there will be more opportunities for FinTechs/banks/international players as regulators and the government are also encouraging new solutions that will boost digital payments.

Adoption of new technologies: CBSL launched a platform to facilitate single-click real-time payments from consumers to merchants via their respective bank accounts. Payments between accounts of different banks, enabled by a common real-time switch, have created major opportunities for real-time payment apps in Sri Lanka. FinTech players can look at developing apps to support these payments in Sri Lanka while also developing similar systems in Bangladesh and Nepal. In Nepal, a leading bank has recently tied up with an international payment network to enable QR-based payments all over the country. Sri Lanka’s issuance of a national standard for QR-based payments has provided a further boost to the QR revolution in the Indian subcontinent. This opens up a range of opportunities for banks and financial institutions to enable QR-based payment apps. The countries should also be open to setting up a regulatory sandbox for FinTech firms to test new and innovative products for greater financial inclusion.

Technology: QR, NFC, real-time payments

Partnerships and collaborations

Digitisation roadmaps

Market updates

Card-issuing giants launch e-wallet in Nepal

UnionPay International announced that it has partnered with SCT, the major card-issuing network in Nepal, in launching an e-wallet product, Qpay. UnionPay thus becomes the first international bankcard association that has launched e-wallet product in the country.

Developed countries round the globe where citizens rely heavily on cashless

Sweden, being the most cashless society in Europe, came second in the list, where 59 per cent of consumer transactions are completed by non-cash methods. UK, the third in the list, is very well aware of alternate payment methods, with 47 per cent saying they know what smartphone payment option they can use.

Bangladesh Bank sets transaction ceiling for contactless card payment

Bangladesh Bank has set per transaction ceiling of Tk 3,000 for the credit cards which would be operated in contactless system also known as near field communication system. The central bank in its circular said dependency on card-based transaction across the country has been on the rise with the evolution of information and communication technology.

COMBANK joins with Alipay to facilitate QR Code based payments for Chinese tourists

This payment channel will be made available through a special Point-of-Sale (POS) device that will be provided to merchants such as gem and jewellery retailers, handicraft shops, tea shops, hotels and restaurants in Sri Lanka

Mobitel launches mCashQR in Sri Lanka

In an effort to drive digital and financial inclusivity, Mobitel recently launched mCashQR, as an additional component to its mCash mobile app. By using a Quick Response (QR) code, users can make transactions with greater speed, ease and convenience.

With inputs from Mihir Gandhi, Ashish Punjabi, Shekhar Lele, Anand Jeyachandran and Tanvi Munjal

Sources

- PwC analysis

- https://theodora.com/wfbcurrent/nepal/nepal_economy.html

- Obtained data from respective countries regulator’s website