Market growth

Third-fastest growing E&M market in CAGR terms (2017–2022)

Video games

Among the top 10 video game markets by 2022 in terms of revenue

E-sports

Highest CAGR for e-sports at 56.6% during 2017–2022

Traditional TV

Strongest CAGR (2017-2022) in India at 10.3%

Overview

PwC's Global Entertainment and Media Outlook 2018–2022 is a comprehensive source of five-year forecast and five-year historic consumer and advertiser spending data and analysis, for 15 entertainment and media segments, across 53 countries. It is a powerful online tool that provides deep knowledge and actionable insights about the trends that are shaping the E&M industry.

Insights from India

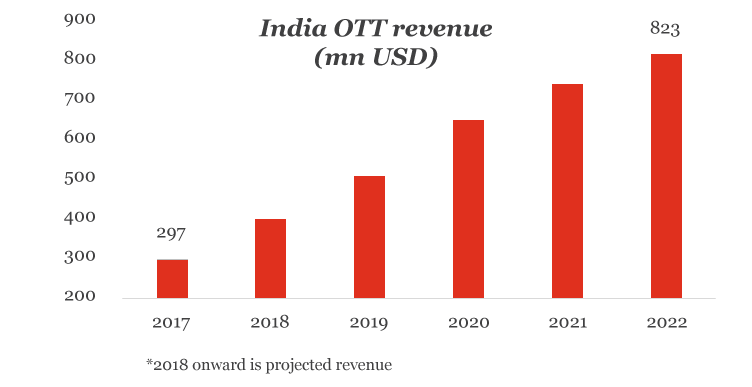

10th largest market for OTT by 2022

India will be the tenth-largest market for OTT in terms of revenue in 2022, with mobile internet subscribers set to double from 406 mn in 2017 to 805 mn in 2022. The OTT video market is being propelled by consumer content demand, lower internet prices and portability preferences. Increased focus on localised content is the key to the Indian OTT market.

Top 10 markets in the world for video games

Large markets without a tradition of gaming - China, India and Russia will account for 41% of social/casual gaming revenue growth from 2017 to 2022. Digital distribution and movement from packaged media to games as services supported by micro transactions are key to growth. New technologies like VR/ AR and ninth-gen consoles are promising innovations in the gaming world. However, revenue contribution from the same will be limited over the next few years.

Highest CAGR (2017 – 2022) in the world with respect to e-sports

The rapid rise of e-sports is being fueled by recurring consumer interest and the increasing attention paid by advertisers and sponsors. At present, favorable demographics – millions of young consumers with increasing levels of disposable income – are making consumer contribution the largest revenue stream.