The time is ripe for the sachet model in financial services

The country has made significant efforts in the area of financial inclusion through various measures such as implementation of schemes, establishment of government-backed institutions, encouragement of differentiated business models such as payments banks and small finance banks, and budgetary announcements. However, metrics across various financial products indicate the need for more innovative solutions to truly transform the underbanked population into under-served, semi-served and fully served.

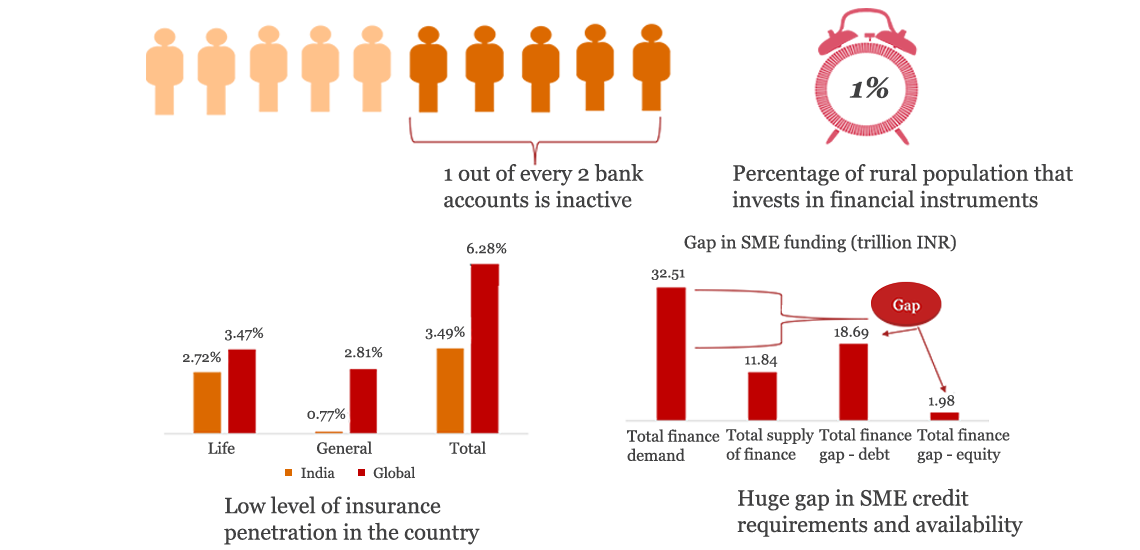

White spaces in the adoption of major financial instruments1

The opportunity

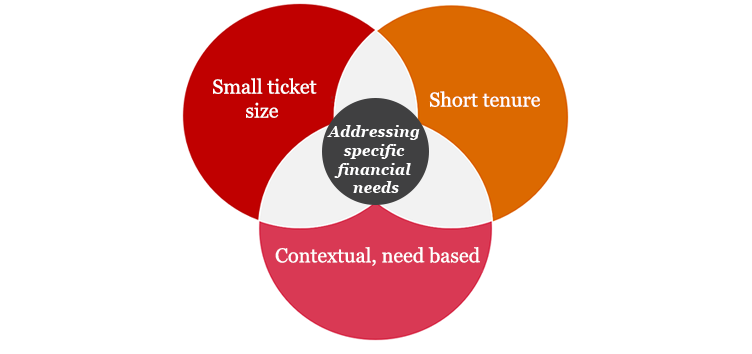

Financial institutions have invested significantly in boosting the last-mile connectivity of their financial products. However, one of the reasons for low adoption of instruments is commoditisation of products. Due to cost economics, products are typically offered in standard pre-defined slabs. And although financial institutions have tried to offer customised products through collaboration with innovative FinTechs, there is definitely ample scope to re-imagine products further. This would typically require the incorporation of some key attributes:

Opportunities to customise financial product offerings

The case for the sachet moment

Small package offerings, commonly referred to as sachets, have transformed a few industries, including fast-moving consumer goods (FMCGs), telecom and direct-to-home (DTH). One of the key objectives of sachet services is to ‘transition from luxury to affordability’. Products and services which were earlier too expensive for the masses are made available in the bare minimum and necessary quantities. There is huge potential to customise financial products. This product differentiation, coupled with enhanced last-mile connectivity and distribution, has the potential to truly transform the way people consume financial services in the country and boost adoption significantly.

The ultimate objective of providing financial services in sachets is to help anyone access any financial product anytime, anywhere and in any quantity, as per the specific requirement.

Specific use cases

The sachet model is suited to for major financial products such as lending, insurance and mutual funds.

Nano-finance

Microfinance has brought about a revolution in the financial services industry by significantly reducing the loan ticket size. However, there are still restrictions on the minimum loan amount that can be issued. This can be further reduced through nano-finance. The illustration below deals with an artisan who has a specific need for a small-ticket loan for a specific duration.

Abbreviations:

POS: Point of sale

GST: Goods and Services Tax

UPI: Unified Payments Interface

DBT: Direct Benefit Transfer

Case study: A mobile phone network provider based out of Haiti2

The firm is looking to leverage its existing mobile money infrastructure to provide its customers with ‘nano-loans’—that is, very small-ticket loans (2–20 USD) for short periods (30 days). It is a mobile money platform that allows its customers to transfer money domestically, pay bills and perform other basic transactions with their mobile phones. The nano-loans will be disbursed and repaid through the platform. This flexibility will give a wider base of consumers access to easy credit with simple repayment options, especially segments that are traditionally underbanked.

Insurance

There is substantial potential for offering insurance products to meet needs in various scenarios.

Case study: Pay-per-day geolocation travel insurance service3

An app-based insurance platform has been developed that provides a pay-per-day travel insurance model which uses a customer’s geolocation to provide instant medical and dental cover at very small premiums starting at less than 1 GBP per day.

The pay-per-day travel insurance leverages mobile app technology to pinpoint a customer’s location and automatically turns on coverage when it’s needed. Users can further customise their insurance easily from their phone while on the move—for instance, by adding winter sports cover or including friends and family on their policy.

On average, a customer is estimated to spend 13 days abroad per year, which as per the pay-per-day offering will cost a user 11.76 GBP a year—which is significantly lower than the costs incurred while availing products from existing insurers. Additionally, to prevent frequent travellers from racking up large insurance bills, there is a cap on the total costs per year or the option to pay a fixed amount for a standard annual travel insurance policy.

Micro-investments

The benefits of investments in mutual funds for long-term wealth creation have been publicised across various media channels. The key to boost investments in financial instruments is to inculcate a savings turned investment habit among people.

Case study: A new age investment platform4

A new type of investment platform aims at empowering small investors who find investing confusing or intimidating.

It makes investing easy and accessible by providing personalised investment recommendations based the on an investor’s response to various questions. Through their mobile platform, investors can invest in a curated selection of exchange traded funds (ETFs) or purchase fractional shares of stocks.

In addition to helping users invest in the companies and sectors that matter most to them and match their interests and beliefs, the mobile app also explains finance and investment concepts in simple terms to help educate users about how to invest. Finally, with a subscription fee of 1 USD per month and a minimum investment value of 5 USD, the platform helps users circumvent the entry barriers traditionally faced by small or first-time investors and makes investments accessible to all.

One of the interesting aspects of sachet services is that they are not restricted geographically (i.e. rural areas) or to the sphere of financial inclusion alone. They can enable multiple services such as account activation, account-related services and micro-transactions which would be region and business segment agnostic. Therefore, it is clear that sachets have huge potential to serve a huge segment of the population through customised low-value, high-volume transactions.

Enabling architecture

The implementation of a sachet service framework to serve the population across the country would require an architecture that is:

- Modular

- Scalable

- Application programming interface (API) driven

- Cloud based

A financial institution should look at building a robust ecosystem along with its partners to enable the processing of a high volume of concurrent transactions across customised product lines and last-mile distribution channels.

Seamless enabling architecture for providing financial services in a sachet

The success of financial services in a sachet would depend upon ease of use, interoperability, real-time decision making and processing, data security, and overall service discovery and fulfilment of needs. It would also require a change in the mind-sets of providers from a push-based approach of offering specific products to a pull-based approach of meeting specific, context-based needs by modifying the core product offerings.

Sources:

1The World Bank. (2017). The Global FinDex Database 2017.

2The Habiri Network (2015). Retrieved from https://www.thehabarinetwork.com/digicel-haiti-relaunches-mobile-money-platform-as-mon-cash (last accessed on 15 May 2018)

3Associated Press. (19 August 2015). Digicel Haiti relaunches mobile money platform as Mon Cash. The Habiri Network. Retrieved from https://www.thehabarinetwork.com/digicel-haiti-relaunches-mobile-money-platform-as-mon-cash (last accessed on 15 May 2018)

4Friedman, Z. (2017). How to invest with just $5. Forbes Retrieved from https://www.forbes.com/sites/zackfriedman/2017/02/02/stash-investment-app/#31181fd969e5 (last accessed on 15 May 2018)